Thank you for contacting

GetTaxReliefNow.com!

We’ve received your information. If your issue is urgent — such as an IRS notice

or wage garnishment — call us now at +(888) 260 9441 for immediate help.

or wage garnishment — call us now at +(888) 260 9441 for immediate help.

Oops! Something went wrong while submitting the form.

OUR SERVICES

Comprehensive Tax Relief Solutions Tailored to You

From IRS Offers in Compromise and penalty abatements to state-level unfiled-returns support, our end-to-end services are customized to resolve your tax debt and restore your financial peace of mind.

IRS Payment Plans for Individuals | Immediate Relief

If you are facing IRS levy action and cannot afford your tax bill, we can help set up an IRS payment plan.

.svg)

Offer in Compromise for Individuals | Immediate Relief

If you are overwhelmed by tax debts and facing wage garnishments or bank levies, we can help you pursue an offer in compromise (OIC).

Currently Not Collectible | Immediate Relief

If you owe income taxes and cannot afford to pay, IRS collection actions can create serious financial pressure.

.avif)

IRS Wage Garnishment Help | Immediate Relief

If you are facing IRS wage garnishment, the Internal Revenue Service may issue a wage levy after a Final Notice of Intent to Levy.

IRS Bank Levy Help |

Immediate Relief

Immediate Relief

If your bank account has been frozen due to IRS bank levies, the Internal Revenue Service may have issued a Final Notice of Intent to Levy.

Federal Tax Lien Resolution | Immediate Relief

A federal tax lien is a public record filed by the Internal Revenue Service when tax debts remain unpaid, attaching to real estate, personal property, and financial assets.

IRS Audit Representation | Immediate Protection

If you received an IRS audit letter, the Internal Revenue Service is reviewing your tax return under federal tax law and the Internal Revenue Code.

.avif)

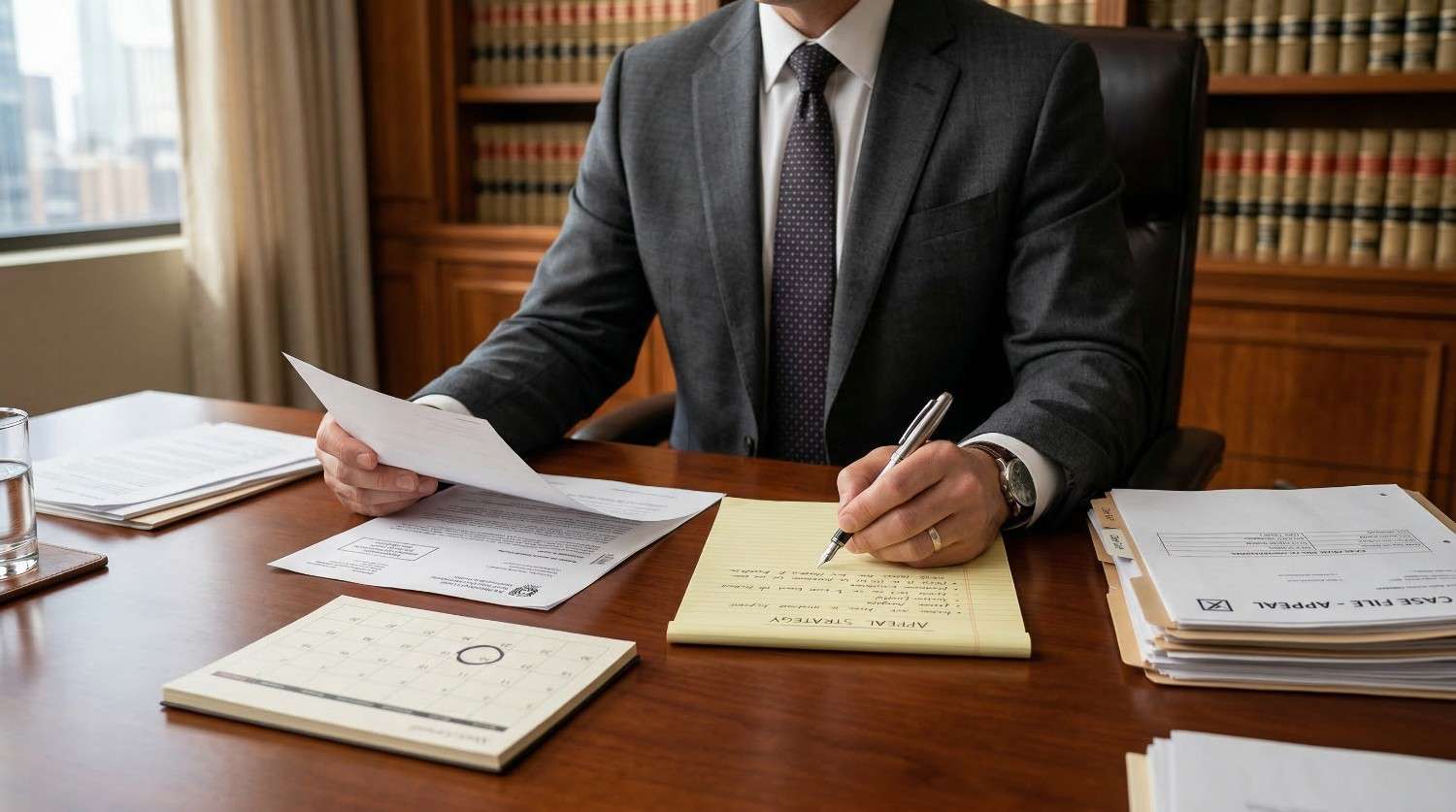

IRS Appeals Representation | Immediate Relief

If the Internal Revenue Service has denied your request or issued a Notice of Deficiency, you may still challenge the decision through the IRS Independent Office of Appeals.

.avif)

Innocent Spouse Relief | Immediate Relief

If the IRS is pursuing tax liabilities tied to a joint return with a former spouse, you may qualify for innocent spouse relief.

.avif)

IRS Collections Representation | Immediate Relief

If you are facing IRS collections for overdue taxes, the Internal Revenue Service may take enforcement action through the IRS collection process.

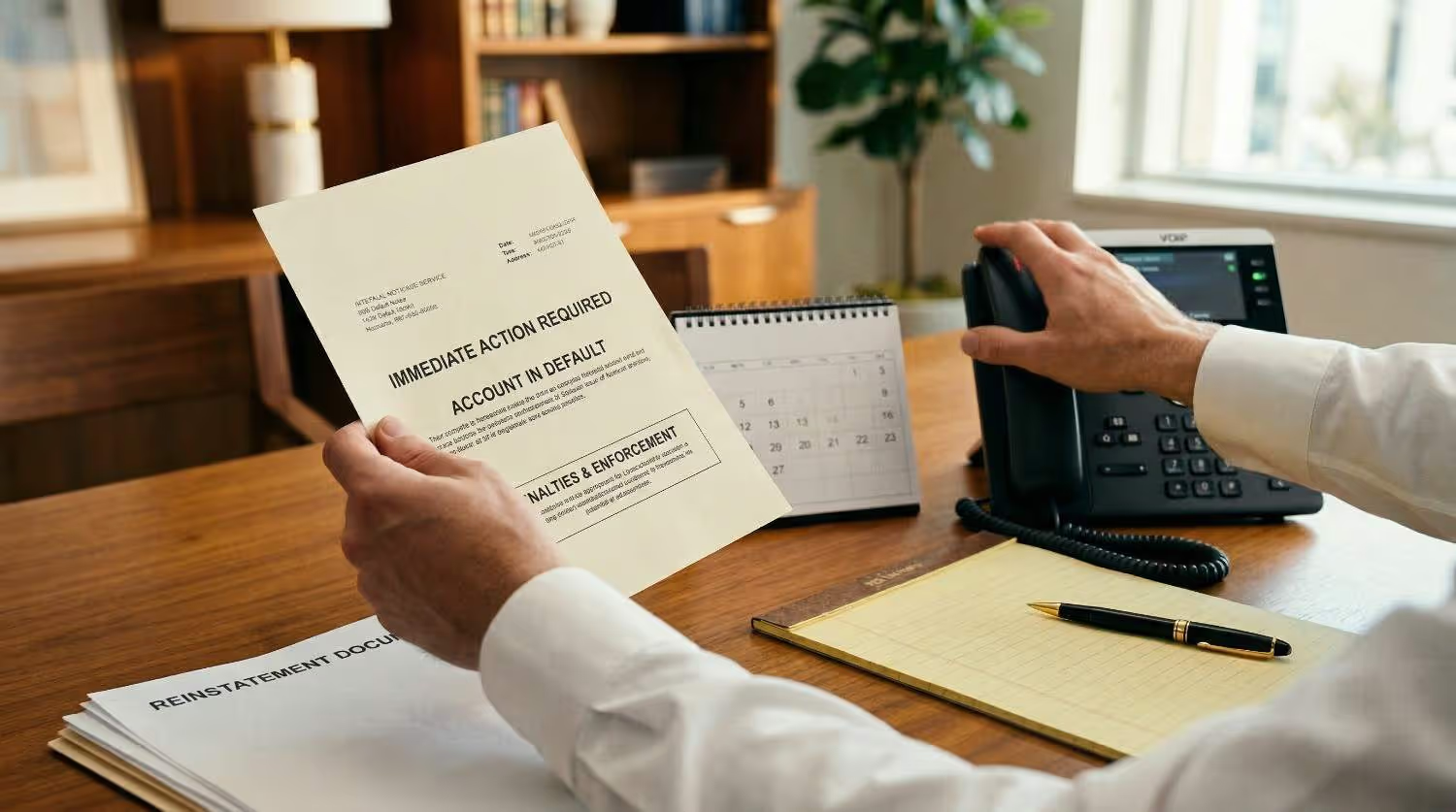

IRS Notice Resolution | Immediate Relief

If you received an IRS Notice, the Internal Revenue Service may be reviewing your tax return, tax account, or federal income tax filings.

Unfiled Individual Tax Returns | Immediate Relief

If you have unfiled tax returns, the Internal Revenue Service may already have income data from Form W-2, Form 1099, or Wage and Income Transcript records.

Back Tax Preparation for Individuals | Immediate Relief

If you have unfiled tax returns, the Internal Revenue Service may flag missing tax filing activity tied to your Social Security Number during tax season.

IRS Transcript Review | Immediate Relief

If you received a balance due notice and do not understand your tax liabilities, an IRS transcript review can clarify your tax account information.

IRS Payment Plans for Businesses| Immediate Relief

If your business owes the IRS and you cannot pay the full balance, you are in a time-sensitive situation. IRS enforcement against businesses moves fast, especially when payroll taxes are involved.

Trust Fund Recovery Penalty Defense | Immediate Relief

If the IRS has contacted you about a Trust Fund Recovery Penalty, you are facing personal exposure for unpaid payroll taxes.

.avif)

IRS Business Bank Levy Help | Immediate Relief

Your business bank account has been frozen, or you just received notice that the IRS intends to levy it. Payroll is due. Vendors are waiting.

IRS Revenue Officer Defense | Immediate Relief

If your business owes the IRS and you cannot pay the full balance, you are in a time-sensitive situation. IRS enforcement against businesses moves fast, especially when payroll taxes are involved.

IRS Audit Representation for Businesses | Immediate Relief

If your business has received an IRS audit notice, you are facing a serious federal examination. An IRS audit is not a routine request for paperwork.

.avif)

IRS Appeals Representation for Businesses | Immediate Relief

If your business has received a 30-Day Letter, 90-Day Letter, audit report, penalty notice, rejected payment plan, or Final Notice of Intent to Levy, you are facing a serious federal tax dispute.

IRS Collections Representation (Business) | Immediate Relief

When your business is in IRS collections, you are not dealing with a typical creditor. The Internal Revenue Service has administrative enforcement power that allows it to levy bank accounts, seize receivables, file federal tax liens, and, in serious cases, shut down operations.

Unfiled Business Tax Returns | Immediate Relief

If your business tax returns remain unfiled, you face the risk of IRS enforcement. IRS enforcement could impact your bank accounts, income, business assets, and personal liability. The letters may already be arriving.

Back Payroll Tax Filings | Immediate Relief

When your business is in IRS collections, you are not dealing with a typical creditor. The If you have unfiled payroll tax returns, you are dealing with one of the most serious enforcement categories at the IRS. Payroll taxes are not treated like ordinary income taxes.Internal Revenue Service has administrative enforcement power that allows it to levy bank accounts, seize receivables, file federal tax liens, and, in serious cases, shut down operations.

State Tax Payment Plans for Individuals | Immediate Relief

If your state says you owe back taxes and you cannot pay the full balance, you are likely under serious pressure.

State Wage Garnishment Help | Immediate Relief

If unpaid taxes are garnishing your wages, you probably feel trapped and overwhelmed. You work hard, yet part of your paycheck disappears before it even reaches your account.

State Bank Levy Help | Immediate Relief

When the IRS freezes your bank account, everything changes overnight. The IRS suddenly locks away money that was available only yesterday.

State Tax Lien Resolution| Immediate Relief

If your state says you owe back taxes and you cannot pay Finding out that the IRS has filed a Notice of Federal Tax Lien against you or your business can feel overwhelming. It is public. It affects your credit.the full balance, you are likely under serious pressure.

State Audit Representation - Individuals | Immediate Relief

An IRS audit can feel like your life just stopped. You open a notice, and suddenly the federal government is questioning your income, deductions, credits, or business records.

Unfiled State Tax Returns | Immediate Relief

If you have unfiled state tax returns, you are not alone. Many individuals and small business owners fall behind during difficult financial periods, health issues, divorce, business downturns, or simple record disorganization.

State Business Tax Payment Plans | Immediate Relief

When your business falls behind on federal tax obligations, the pressure can feel immediate and overwhelming.

State Payroll Tax Problems | Immediate Relief

Payroll tax problems can feel overwhelming, especially when IRS notices start arriving, and the language becomes more urgent.

State Business Bank Levy Help | Immediate Relief

When the IRS levies your business bank account, the disruption is immediate. Payroll may fail. Vendor payments may bounce.

State Audit Representation for Businesses | Immediate Relief

An IRS business audit can disrupt your operations overnight. You may be focused on payroll, vendors, customer service, and growth when suddenly a formal IRS notice demands records, explanations, and strict deadlines.

Unfiled State Business Tax Returns | Immediate Relief

When your business has unfiled state tax returns, and the IRS is already sending notices, the pressure can feel constant.

Defaulted IRS Payment Plans | Immediate Relief

If your IRS payment plan has defaulted, you are no longer in a protected position. What once shielded you from aggressive collection may no longer be in place.

Rejected Offer In Compromise | Immediate Relief

If the IRS rejected your offer in compromise (OIC), you probably feel frustrated, discouraged, and anxious about the next steps.

Multi-Year Back Tax Problems | Immediate Relief

When you owe the IRS for multiple years, the problem rarely stays contained. Penalties and interest continue to grow.

IRS Enforcement Defense | Immediate Relief

If the IRS has started sending certified letters threatening to levy your bank account, garnish your wages, or file a notice of federal tax lien, you are not just dealing with paperwork.

Emergency IRS Action Help | Immediate Relief

When the IRS begins enforcement, it does not feel routine. It feels urgent and personal. A wage levy can reduce your paycheck without warning.

Penalty Abatement Services | Immediate Relief

If you are dealing with IRS penalties, you already understand how quickly they can spiral. A missed filing deadline, an unpaid tax balance, or a payroll deposit issue can trigger penalties that grow month after month.

Tax Planning for Individuals | Immediate Relief

If you are receiving IRS notices, facing a growing balance, or worried about wage garnishment or bank levies, it can feel like your finances are under constant threat.

Tax Planning for Businesses | Immediate Relief

When your business is under pressure from the Internal Revenue Service, tax planning is no longer just about future savings.

Substitute for Return (SFR) Defense | Immediate Relief

When your business is under pressure from the Internal Revenue ServiIf the IRS filed a tax return for you, the situation is already serious. A substitute for return (SFR) means the IRS prepared a return on your behalf because you did not file one yourself.ce, tax planning is no longer just about future savings.

High-Balance Tax Debt Cases | Immediate Relief

If you owe a high balance to the IRS, you are likely feeling intense pressure. The notices may be arriving more frequently.

Multi-State Tax Problems | Immediate Relief

When your business is under pressure from the Internal Revenue Service, tMulti-state tax problems can feel overwhelming very quickly. You may have moved to a new state, but you still receive tax bills from your previous state.ax planning is no longer just about future savings.

Payroll Tax Personal Liability | Immediate Relief

When payroll taxes fall behind, the situation can turn serious very quickly. What starts as a cash flow problem inside your business can become a direct personal threat.

Unfiled Federal and State Tax Returns | Immediate Relief

Falling behind on tax returns can happen slowly. One missed year turns into two. Then life gets busy, business gets complicated, records get lost, and fear sets in.

IRS Levy Release Timing | Immediate Relief

When the IRS levies your bank account or starts garnishing your wages, the impact is immediate.

Frequently Asked Questions (FAQs)

Can I still get a refund?

Can I still file my 2011 Form 1040?

Do I need a lawyer or tax professional to respond to an IRS intent to levy?

What if the IRS levy causes immediate financial hardship?

Can the IRS issue multiple tax levies on the same account?

Please let me know how long it typically takes to release an IRS levy.

What happens if I ignore an IRS Notice of Intent to Levy?

Can the IRS levy a joint bank account?

How does a bank levy differ from a wage garnishment for tax debt?

How can I ensure my filing information is accurate before submission?

Ready to Get Started?

Don’t miss out on valuable tax relief. The sooner you apply, the sooner you may receive

reduced tax bills, lower payments, and possible refunds.

reduced tax bills, lower payments, and possible refunds.

Get A State Tax Relief Review