IRS CP and LT notices are official letters that the IRS sends to taxpayers about their accounts. These notices highlight unpaid balances, unreported income, or discrepancies between tax returns and IRS records. Each notice has a code, such as CP504 or LT11, which signals a specific tax problem. Understanding the notice type helps taxpayers determine the seriousness of the issue and possible IRS levy actions.

Taxpayers usually receive these notices because the IRS detected an error, a missing payment, or an unresolved tax debt on their account. For example, a CP2000 notice proposes changes if reported income does not match IRS records. An LT11 or Letter 1058 may warn of an intent to levy wages or assets. These IRS notices are direct signals that immediate attention and response are necessary.

Timely action is crucial because ignoring a notice can trigger levy actions, additional penalties, or even a federal tax lien. Responding promptly allows taxpayers to protect wages, property, and credit from harsh IRS collection steps. Fortunately, the IRS provides collection alternatives, including payment plans, appeals, or settlement programs. Professional tax help ensures taxpayers understand their options and successfully navigate collection due process hearings.

What Are CP and LT Notices and IRS Notice Types

It is essential to understand CP and LT notices because they explain how the IRS communicates tax issues, payment demands, and potential enforcement actions.

- CP Notices Explained: CP (Computer Paragraph) notices are IRS notices automatically generated by the IRS system to inform taxpayers about issues such as underreported income, unpaid balances, or proposed adjustments.

- LT Notices Explained: LT (Letter) notices are more formal IRS letters that often serve as the final communication before serious enforcement, including an intent to levy or filing a federal tax lien.

- Connection to Levy Actions: If you fail to respond or resolve your tax balance, both CP and LT notices may warn of levy actions, such as an IRS levy against wages or bank accounts.

- Role in Collection Due Process: Certain notices, including an LT11 or Letter 1058, trigger your right to request a collection due process hearing (CDP hearing), which allows you to challenge or negotiate the IRS’s intent to levy.

- Why Recognition Matters: Recognizing IRS notices like Letter 1058 is critical because failing to act promptly can lead to additional penalties, the loss of your collection due process rights, and fewer collection alternatives.

- How to Respond: If you receive a CP or LT notice, you should contact the IRS immediately or seek professional help to explore collection alternatives, request a CDP hearing, or prevent further levy actions.

By understanding CP and LT notices and acting quickly, you can protect your rights, reduce additional penalties, and keep more collection alternatives open.

Common Types of Notices and Intent to Levy Letters

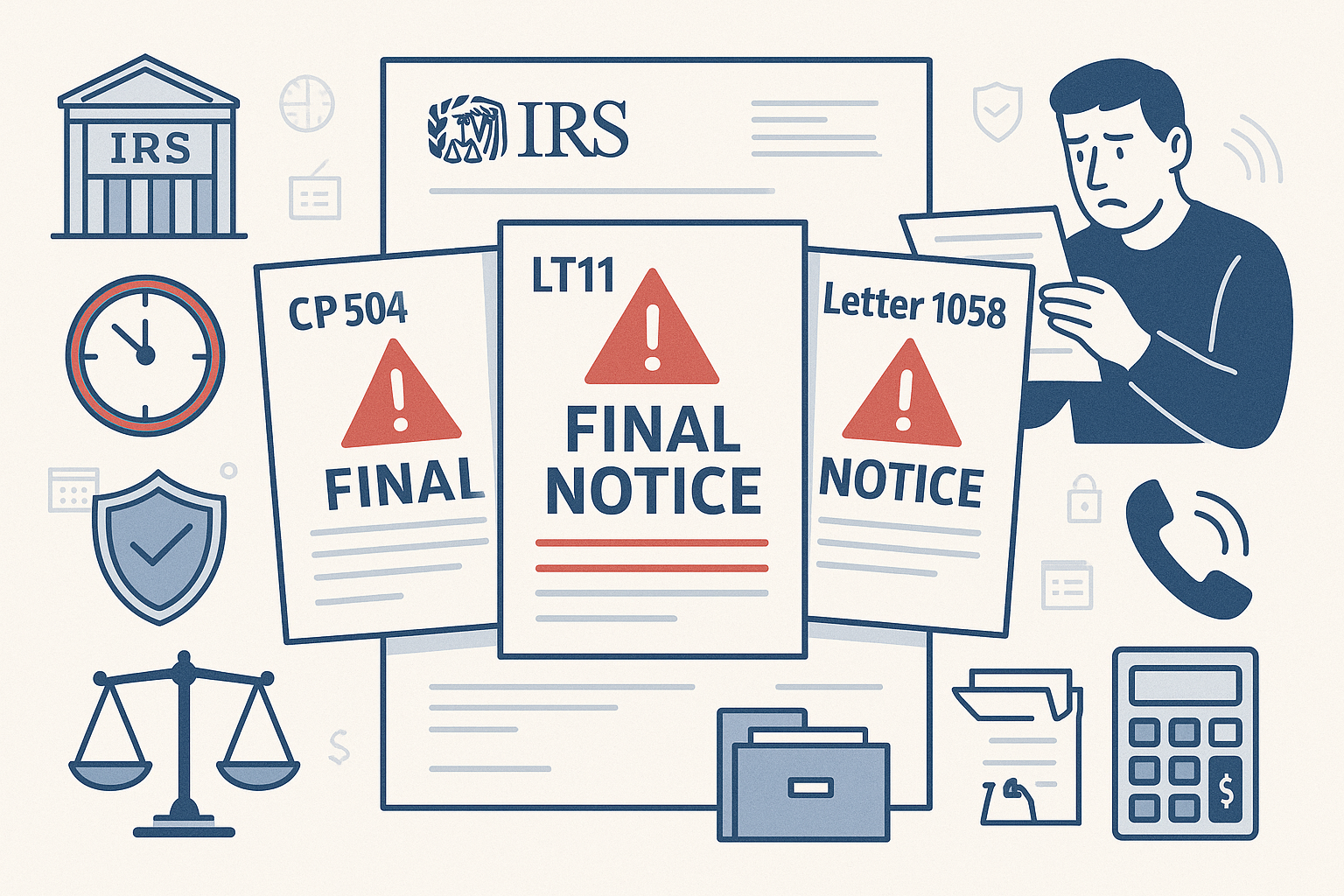

Understanding CP and LT notices is essential because each carries different consequences and deadlines. Below, we summarize the most common IRS notices, their meaning, and how taxpayers can respond before facing levy actions or additional penalties.

CP504 – Final Notice of Intent to Levy

What it means and potential levy actions if ignored:

- Serious escalation: The CP504 is an IRS notice informing you of the government’s intent to levy your state tax refund and begin levy actions if the debt is not addressed.

- Limited response window: You generally have 30 days to respond before the IRS levy process starts.

- Consequences of inaction: If ignored, this notice can lead to aggressive levy actions on wages, bank accounts, or other assets.

Connection to federal tax lien enforcement:

- Notice of lien filing: Ignoring a CP504 can result in the IRS filing a federal tax lien against your property, which secures the government’s claim on your assets.

- Impact on credit: A federal tax lien can harm your ability to obtain loans, mortgages, or credit cards.

- Collection alternatives: To prevent a lien, you can contact the IRS to request collection alternatives such as an installment agreement or an Offer in Compromise.

CP2000 – Proposed Changes to Tax Return

Why it’s issued as an IRS notice:

- Mismatch in records: A CP2000 is sent when IRS records do not match the income or payment details reported on your tax return.

- Not an audit: Although it looks serious, this IRS notice is not a formal audit but a proposed adjustment.

- Potential penalties: If unaddressed, the changes can lead to additional penalties and interest.

What to do if you disagree, including requesting a collection due process hearing if applicable:

- Review the details: Compare the IRS’s information with your tax records to verify accuracy.

- Respond quickly: Contact the IRS with supporting documents to challenge the proposed changes if you disagree.

- Seek due process: In certain situations, you may have the right to request a collection due process hearing (CDP hearing) to dispute the adjustment formally.

- Explore alternatives: If you owe after the adjustment, ask about collection alternatives to resolve the balance.

LT11 – Final Notice of Intent to Levy

Key differences from CP504:

- Direct warning: Unlike CP504, LT11 is a final IRS notice that warns of immediate intent to levy wages, bank accounts, or property.

- Appeal rights: The LT11 outlines your right to request a CDP hearing before levy actions begin.

- Time-sensitive: Ignoring LT11 can result in faster enforcement compared to CP504.

How it relates to CDP hearings and collection alternatives:

- CDP hearing opportunity: LT11 gives you the right to request a collection due process hearing, which allows you to appeal the IRS levy and present your case.

- Collection alternatives: During the CDP hearing, you can propose alternatives such as an installment agreement, Offer in Compromise, or temporary hardship status.

- Avoiding escalation: Proactively addressing the LT11 notice helps prevent federal tax lien filings and additional penalties.

Reference to Other Common Notices like Letter 1058

What Letter 1058 means:

- Equivalent to LT11: Letter 1058 is another final IRS notice of intent to levy, giving you the same rights as the LT11 to request a CDP hearing.

- Formal warning: It signals that legal actions are imminent unless you take action.

- Next steps: Contact the IRS immediately to discuss collection alternatives or request a collection due process hearing.

CP and LT notices such as CP504, CP2000, LT11, and Letter 1058 are crucial warnings from the IRS. Ignoring them can lead to levy actions, additional penalties, or a federal tax lien. By understanding what each notice means and exercising your rights to contact the IRS, request a CDP hearing, or pursue collection alternatives, you can protect your assets and resolve your tax situation before it escalates.

Why You May Have Received a CP or LT Notice

When you receive CP or LT notices, it usually means the IRS has identified issues with your account that require immediate attention. These are some of the most common reasons taxpayers face these notices.

- Unpaid or Underpaid Taxes: The IRS sends CP LT notices when you owe back taxes or underpaid your obligations, which may trigger an intent to levy if you do not act promptly.

- Discrepancies in IRS Records: A mismatch between your filed return and the IRS records can result in an IRS notice such as CP2000, which, if ignored, may escalate to levy actions.

- Failure to Respond to Previous Notices: Ignoring earlier correspondence, including Letter 1058, can lead to additional penalties, aggressive levy actions, and the loss of your right to request a collection due process hearing.

- Risk of a Federal Tax Lien: If balances remain unpaid, the IRS may file a federal tax lien, limiting your collection alternatives and making it critical to contact the IRS or request a CDP hearing to protect your rights.

Understanding why you received a CP or LT notice helps you take the right steps, whether through a collection due process appeal, exploring collection alternatives, or working directly with the IRS to resolve the issue before it escalates further.

What To Do When You Receive a Notice from the IRS

When you receive a notice from the IRS, taking immediate and informed action can help you avoid additional penalties, levy actions, or even a federal tax lien. Here are the key steps to follow:

- Carefully Review the IRS Notice: Read the notice line by line to identify whether it includes intent to levy language or warnings about levy actions. Also, please note any deadlines the IRS has set.

- Compare Against Your Tax Records: Match the information in the notice with your filed tax return, W-2s, or 1099s to confirm whether the IRS is correct or if there are discrepancies you can dispute.

- Contact the IRS Promptly: Call the IRS using the number on the notice to ask questions, confirm your balance, and discuss collection alternatives such as installment agreements or temporary relief options.

- Seek Professional Guidance for a CDP Hearing: If the notice mentions your right to a collection due process hearing, consult a tax professional or attorney to help you file a timely request and prepare a strong defense.

By taking these steps immediately, you can protect your rights, reduce enforcement risks, and keep more options open for resolving your tax issue.

Resolution Options for CP and LT Notices

When the IRS sends CP or LT notices, your tax debt is overdue, and collection efforts are escalating. These notices, such as CP504, LT11, or Letter 1058, often warn of enforced collection actions, including levy actions, a federal tax lien, or seizure of personal property and business assets. Below are the main resolution options to stop enforced collection and protect your financial situation.

Pay Your Balance in Full to Stop Levy Actions

If you can afford it, paying the initial amount you owe in full is the fastest way to resolve CP and LT notices and end IRS claims.

- Immediate Relief: Paying your overdue taxes in full stops enforced collection actions such as levy notices on bank accounts, other income, or social security benefits.

- Avoid Additional Penalties: A full payment eliminates interest growth and additional penalties for delinquent tax debt.

- Release of Tax Lien: Once the tax debt is satisfied, the IRS generally releases the notice of federal tax lien, clearing public notice of your unpaid taxes.

Paying in full ensures the IRS closes your case quickly and prevents future enforced collection actions.

Request a Payment Plan or Installment Agreement

If you cannot pay in full, request a payment plan through the IRS Independent Office of Appeals or apply online.

- Installment Agreement: An installment agreement allows you to make monthly payment arrangements until the amount you owe is fully satisfied.

- Flexible Payment Options: Depending on your financial situation, you may qualify for short-term or long-term payment options, which can help avoid enforced collection.

- Protect Current Assets: Setting up a payment plan shows good faith, which can prevent levy actions against your personal assets and business assets.

By requesting a payment plan, you intend to resolve your tax debt, which can halt collection efforts and ease financial stress.

File for Penalty Abatement

If additional penalties make your tax debt unmanageable, you may qualify for relief.

- First-Time Abatement: The IRS may remove penalties if you have a clean tax return history and this is your first delinquent tax debt.

- Reasonable Cause: Circumstances such as serious illness or natural disasters may support your request for penalty abatement.

- Reduced Balance: Successful abatement lowers the initial amount you owe and can make payment arrangements more manageable.

Penalty abatement reduces the burden of delinquent tax debt, making repayment more realistic.

Apply for an Offer in Compromise

An Offer in Compromise lets you settle your tax debt for less than the full amount if paying in full would create severe financial hardship.

- IRS Review: The IRS Independent Office examines your financial situation, current assets, other property, and other income bank records to determine eligibility.

- Eligibility Factors: The IRS considers your ability to pay, income, expenses, and the value of your personal property and business assets.

- Act Legislation Connection: Under the Fixing America’s Surface Transportation Act legislation, settling your debt can prevent passport certification that may otherwise restrict your United States passport.

An Offer in Compromise provides a fresh start if paying in full or through a payment plan is not feasible.

Request a CDP Hearing or Explore Other Collection Due Process Protections

You have the right to a Collection Due Process hearing if you receive a final notice, such as a Notice of Intent to Levy, sent by certified or registered mail.

- Independent Review: A CDP hearing through the Independent Office of Appeals reviews whether IRS levy actions or a federal tax lien were appropriate.

- Protect Your Rights: The hearing allows you to challenge enforced collection actions and request collection alternatives.

- Legal Path: If you disagree with the decision, you can appeal to the tax court or request an equivalent hearing.

A CDP hearing ensures that enforced collection actions respect the Internal Revenue Code and your taxpayer rights.

Pursue Collection Alternatives to Prevent a Federal Tax Lien or IRS Levy

When dealing with delinquent tax debt, you can seek alternatives that reduce the impact on your financial situation.

- Collection Alternatives: Options include amended returns, payment arrangements, or contacting a tax professional to explore customized solutions.

- Protect Property: Alternatives may prevent seizure of personal assets, Alaska Permanent Fund dividends, state tax refunds, or other income.

- Resume Payments: Demonstrating willingness to resume payments can help avoid enforced collection and IRS levy actions.

Exploring collection alternatives may provide breathing room while addressing the tax debt under the Internal Revenue Service's hearing framework. IRS CP and LT notices signal serious collection efforts under the Internal Revenue Code, but multiple resolution options exist. Whether you pay in full, request a payment plan, apply for penalty relief, or pursue collection due process protections, each option helps you avoid enforced collection and regain control of your financial future. Acting promptly and, when necessary, working with a tax professional ensures the best outcome for resolving your delinquent tax debt.

How We Can Help with IRS Notices and Levy Actions

When you receive an IRS notice, it can feel overwhelming and urgent. Our team offers targeted support to protect your rights and resolve your tax issues effectively.

- Explain Complex CP and LT Notices Clearly: We explain IRS notices such as CP504, CP2000, LT11, and Letter 1058 in plain language so you understand exactly what the IRS is demanding and your next steps.

- Assist in Preparing for a CDP Hearing or Collection Due Process Appeal: We guide you through requesting and preparing for a collection due process (CDP) hearing, ensuring that you meet deadlines and present strong arguments for relief or alternative solutions.

- Represent You in Negotiations with the IRS for Collection Alternatives: We advocate on your behalf in discussions with the IRS, pursuing collection alternatives such as installment agreements, offers in compromise, or temporary hardship status.

- Help Stop Levy Actions, Federal Tax Lien Filings, and Additional Penalties: We act quickly to halt levy actions on your wages or bank accounts, prevent or remove federal tax liens, and reduce exposure to additional penalties through proactive negotiation and compliance strategies.

With our support, you can take control of the situation, protect your assets, and work toward a resolution that minimizes financial and legal consequences.

.png)