Business Tax Relief

Business Tax ReliefTax penalties and debt can escalate quickly if ignored, but the IRS and state agencies offer relief options such as penalty reductions, settlements, and payment plans for eligible taxpayers.

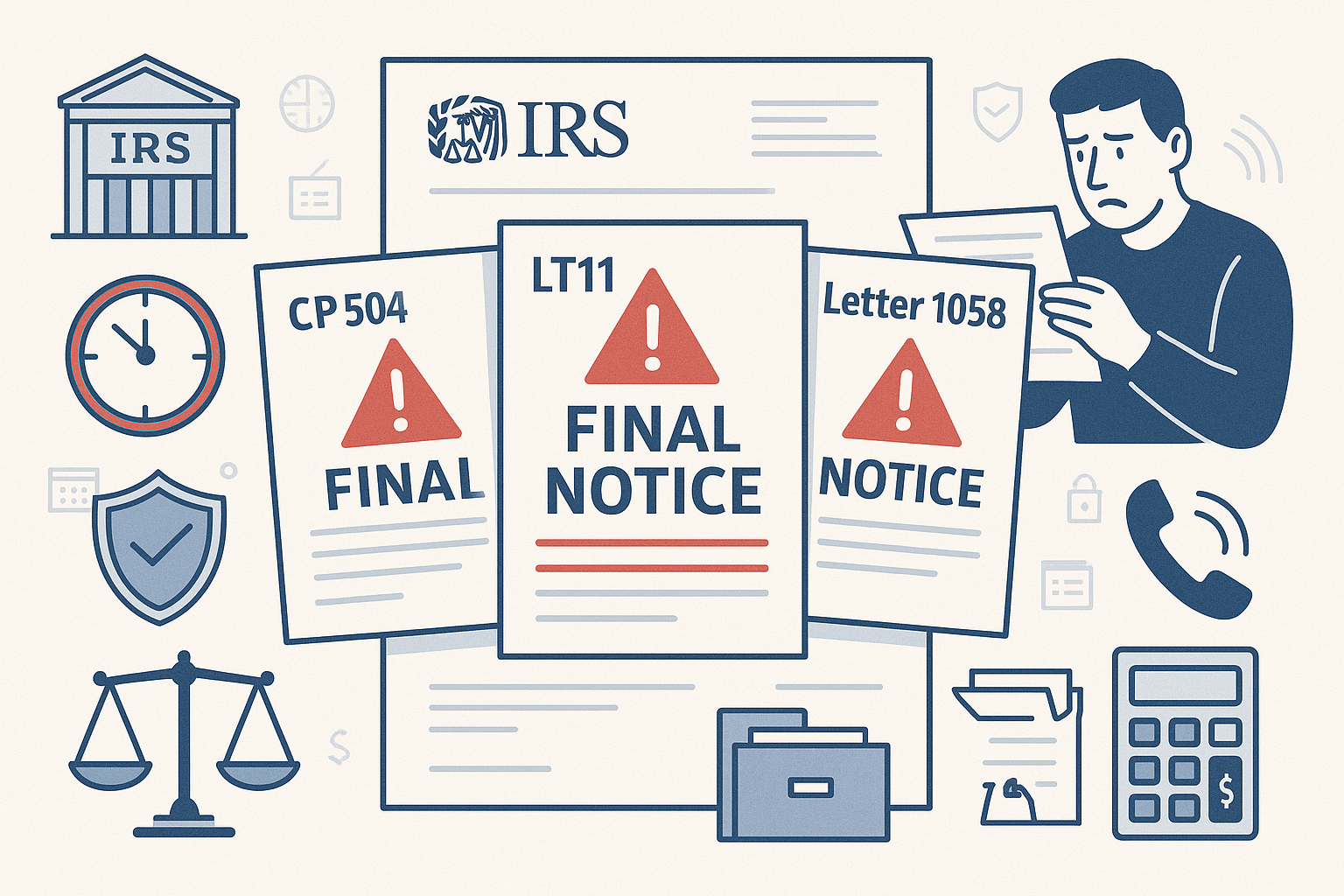

CP & LT Notices

CP & LT NoticesIRS CP and LT notices inform taxpayers about account issues like unpaid balances, unreported income, or return discrepancies. Each coded notice (e.g., CP504, LT11) indicates a specific problem, helping taxpayers gauge its seriousness and potential levy actions.

IRS Collection Process

IRS Collection ProcessThe IRS collection process is a structured system for recovering unpaid taxes. It begins after tax assessment and escalates through enforcement measures until the debt is resolved, paid, or deemed uncollectible. Knowing your rights, the timeline, and available resolution options is key to protecting assets.

IRS Form Help Center

IRS Form Help CenterThe IRS Form Help Center provides resources to simplify federal tax filing. It explains forms, instructions, and deadlines clearly, reducing stress and confusion. Whether you need a specific form or step-by-step guidance, the center helps taxpayers approach tax season with confidence.

IRS Offer in Compromise

IRS Offer in CompromiseAn IRS Offer in Compromise lets taxpayers settle their tax debt for less than the full amount owed. It provides a legal resolution, helps protect essential living funds, and offers a structured path to resolve overwhelming tax liabilities.

IRS Payment Plans

IRS Payment PlansAn IRS payment plan is one of the most effective defenses against bank levies when dealing with tax debt. By setting up a plan, taxpayers gain legal protection for their bank accounts while making manageable monthly payments. Acting quickly to establish an installment agreement helps preserve essential funds for living expenses and provides a structured path to resolve tax obligations.

IRS Penalty Abatement

IRS Penalty AbatementIRS penalty abatement is a relief program that lets eligible taxpayers request removal or reduction of penalties for compliance failures. It helps save money and resolve tax liabilities, especially when circumstances beyond a taxpayer’s control prevented timely compliance.

IRS Power of Attorney

IRS Power of AttorneyAn IRS Power of Attorney authorizes a qualified professional to act on your behalf in tax matters. It ensures protection during audits, disputes, and reviews by allowing experts to handle communication with the IRS. Without it, you must personally manage all interactions.

Innocent Spouse Relief

Innocent Spouse ReliefInnocent Spouse Relief protects individuals from unfair tax debt caused by a spouse’s errors on a joint return. It allows taxpayers to avoid sole responsibility for unreported income or incorrect deductions made by their partner, ensuring fairness in joint liability cases.

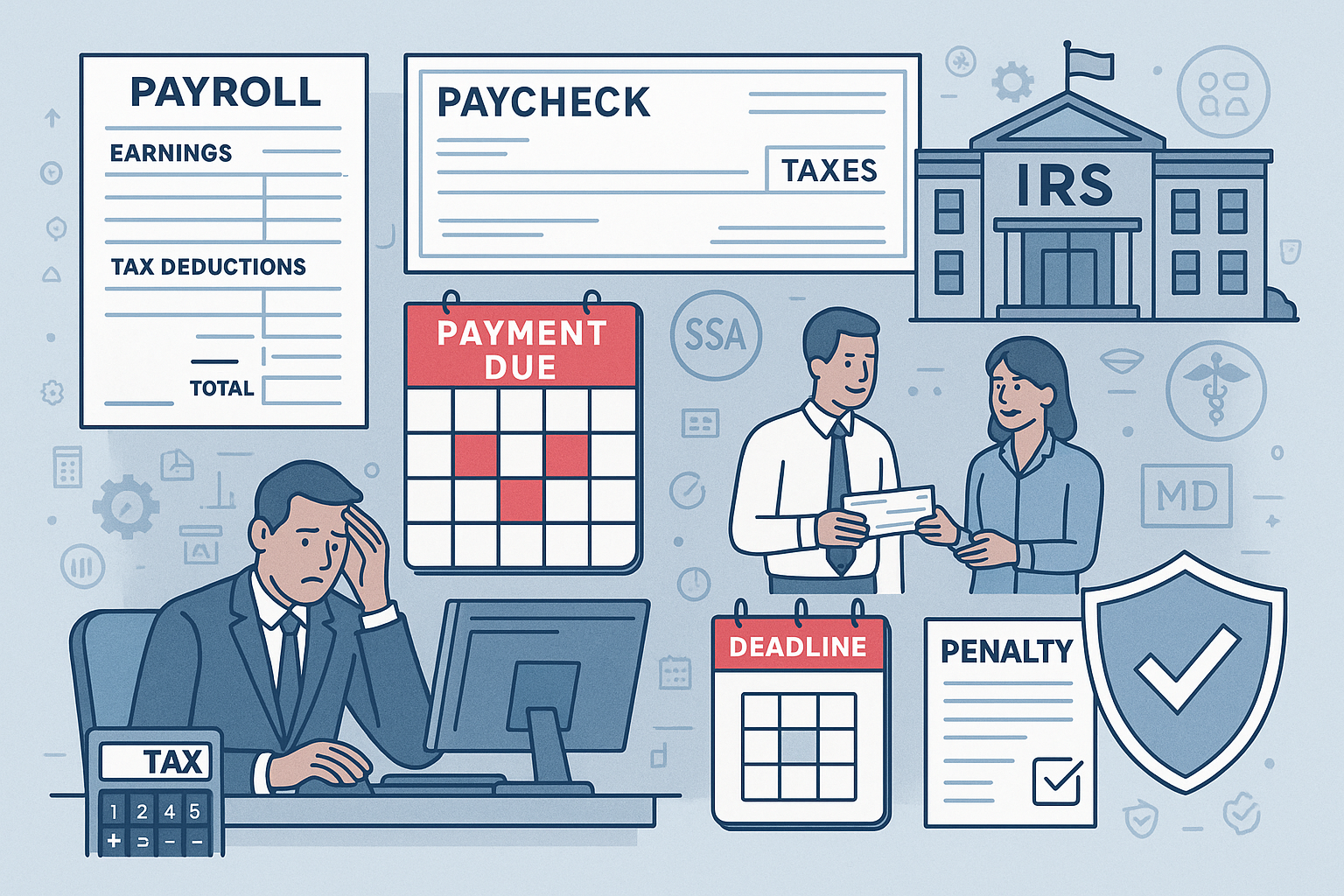

Payroll Tax Issues

Payroll Tax IssuesPayroll taxes are required withholdings from employee wages that fund Social Security, Medicare, and unemployment programs. They provide vital benefits for retirement, disability, and job loss. Employers must manage them accurately to avoid penalties and maintain employee trust.

Unfiled Federal Returns

Unfiled Federal ReturnsUnfiled tax returns can result from financial, health, or paperwork challenges. However, delaying worsens consequences—penalties, substitute returns, and aggressive collection actions like wage or account garnishment.

Wage Garnishment Protection

Wage Garnishment ProtectionA wage garnishment allows creditors or government agencies to take money directly from your paycheck to cover unpaid debts, such as taxes. If you are facing a garnishment, it is important to know that you have rights and options for relief.

Our priority, and we're committed to offering thorough responses to ensure you have the information you need to move forward with confidence.

Schedule your confidential tax relief review today

Copyright © 2025 Get Tax Relief Now